On My Mind

The situation in the ME keeps markets quite busy. While overall indices are down barely 10% I see much greater declines in single names or at least the ones I am watching closely. I will get into more details in the portfolio update that I will publish at the beginning of April. I think of companies like Visa, Mastercard, Thermo Fisher, Danaher, Microsoft, Booking, S&P Global, Berkshire Hathaway, Intuit, Chipotle, Uber and many more.

These are no value picks trading at a P/B of 0.5 but certainly these businesses are of (at least previously perceived) very high quality. Still, they are trading at the lowest valuations in years. I read an article on X this week about Guy Spier closing down his fund due to health reasons, and I believe somebody commented something in the sense of: stock picking is dead.

I do not think it is dead. Even with all the information that is available to individuals, institutional investors, algorithms, markets are always the result of human psychology and emotions. I think running a portfolio of 15 or 30 stocks and trying to outperform the market with large caps is dead, and it always was. Is it possible with only 5 or 6 individual stocks? Absolutely.

This is not the way I invest here at The Tiny Family Office, as I have a different mandate and investment goal, but sometimes I feel the urge to sell it all, just buy 5 great businesses, and never look back. As Charlie Munger used to say: putting all eggs in one basket and watch it carefully.

Worth Noting

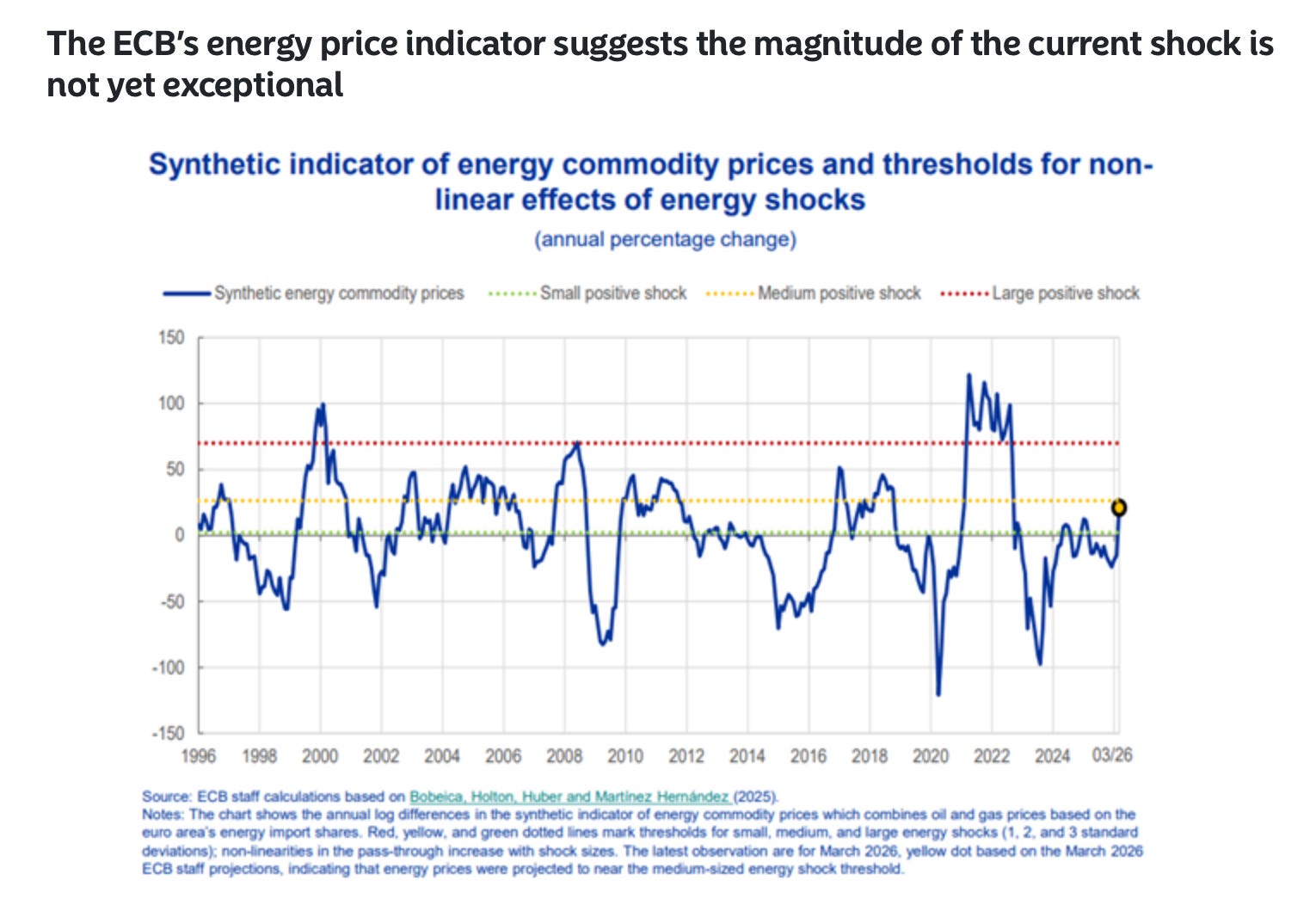

Nordea published another interesting piece with the title “Macro & Markets: Will higher energy prices alone justify hiking rates?”

Europe and Asia are perceived to be more vulnerable to prolonged energy prices than the U.S.. Slowing economic activity across one region will also affect other regions with spill-over effects. So yes, the U.S. economy is shielded but not immune. The big question is if central banks will have to hike interest rates. According to the chart above taken from Nordea’s research this would not be the case for Europe at the moment. Especially because economic activity is already slowing down globally across PMIs, consumer confidence and with higher inflation expectations. Lower asset prices also have an effect on that.

Nordea writes:

“While we are on the verge of moving our baseline ECB hikes from 2027 clearly forward, we have not done so yet. We still tend to think it would be easier for the ECB to wait at least until the June meeting for better visibility on the how the situation in the Middle East evolves, how the economy reacts to the higher prices, what is the response from fiscal policy and, most importantly, how higher energy prices feed through to other prices and inflation expectations. Further, a full set of staff forecasts would be available at the June meeting.”

As you know I am not a big fan of acting on macro research, and I think predicting short-term movements of economies, interest rates or currencies does not really matter if you invest for the long-run. I can spoiler a tiny fraction of the portfolio update for March already: I barely did anything.

I am certain we have another interesting week ahead of us.

Thank you for reading along.