Performance Review

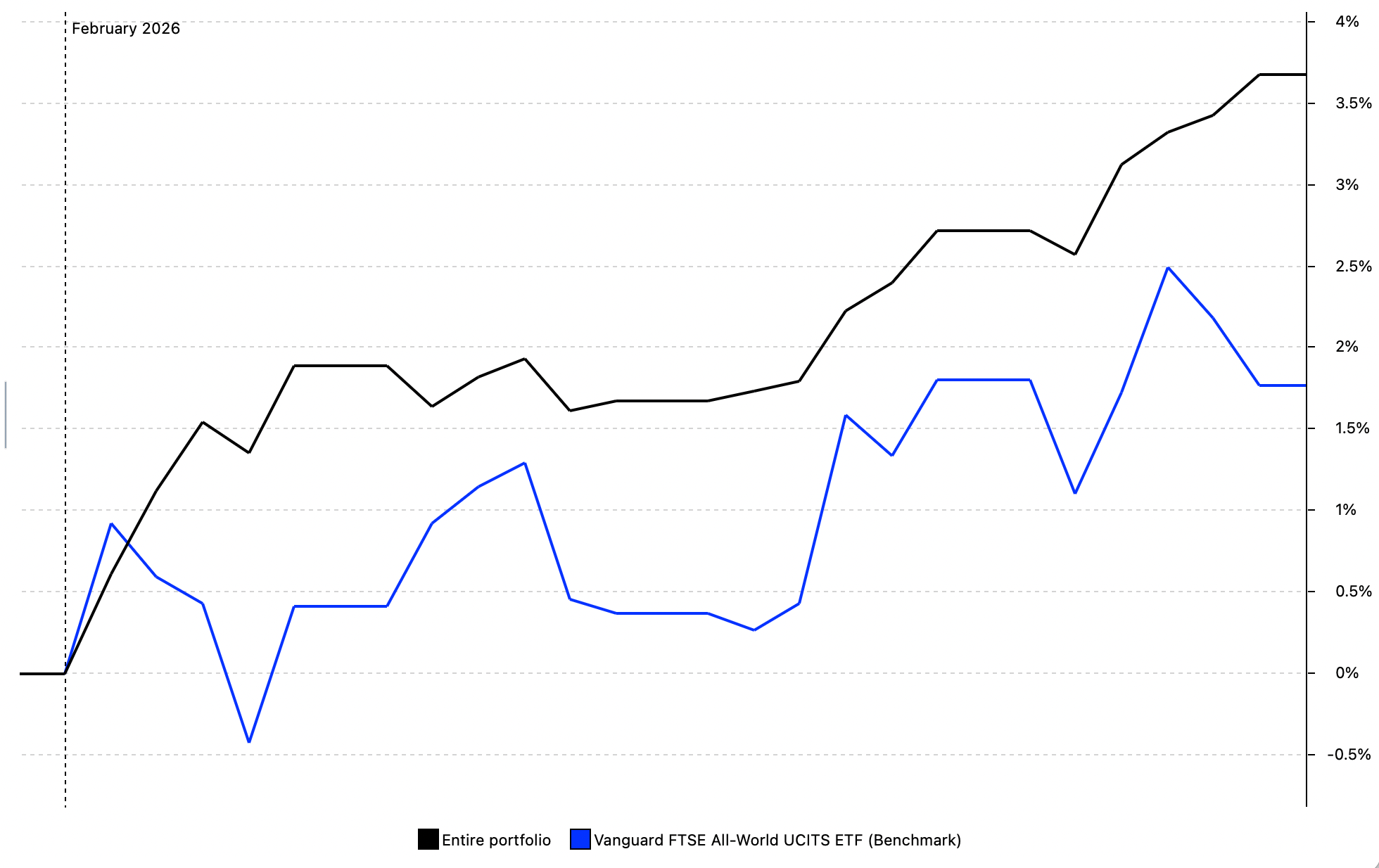

The portfolio returned 3.71% in February 2026. YTD the portfolio is up 4.40% outperforming even an all-equity benchmark like the Vanguard FTSE All-World.

The long-term objective is to compound capital at approximately 7–8% annualized over a full cycle, while limiting drawdowns to a level that allows disciplined decision-making during periods of stress.

Top contributors / detractors during the month:

Contributors: Nestlé, Global Equities (Vanguard FTSE All-World), Berkshire Hathaway

Detractors: Visa, Magnum Ice Cream Co, RIT Capital Partners

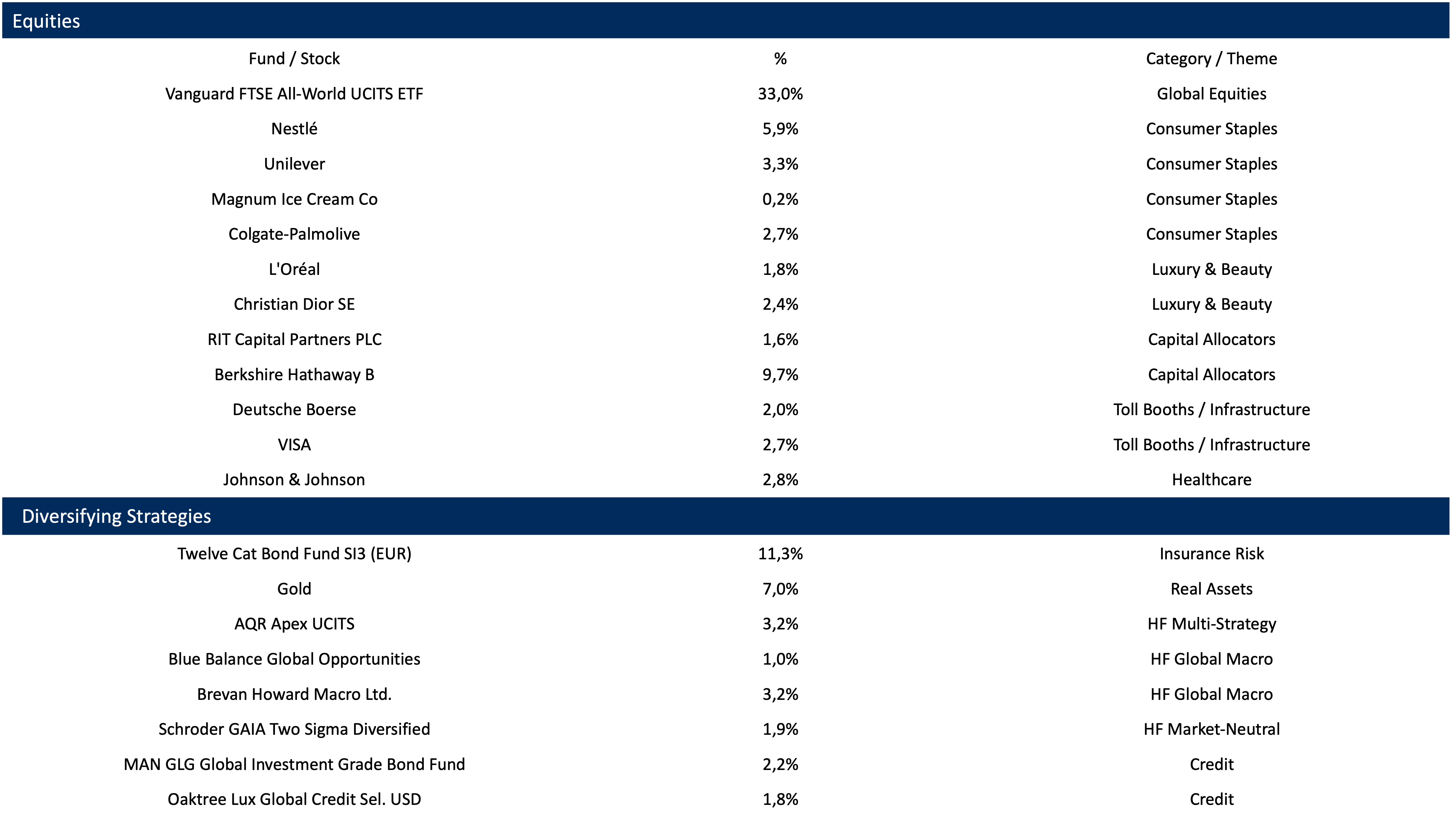

Asset Allocation

Commentary

The portfolio ended the month with an allocation of 68% equities and 32% diversifying strategies.

I could make it short here and just say that January’s top detractors became February’s top contributors. The portfolio performed very well across all segments with only 4 positions being down during February. The substantial exposure to the consumer staples sector (>12%), and the 7% allocation to Gold provided the intended diversification against global equity indices. Especially as technology-related sectors were impacted by fears of disruption through AI. The chart below shows the portfolio compared to an all-equity benchmark.

While I am happy about the performance in February, I am well aware that the high exposure to the staples sector will become a drag once technology-related sectors recover or initiate a new bull market.

JNJ Update

Johnson & Johnson published its 2025 Annual Report this month, with a few positive pipeline news. The company announced a $1 billion investment to expand its cell therapy manufacturing footprint in Pennsylvania, aiming to scale its oncology portfolio. JNJ secured a notable FDA approval for Rybrevant Faspro and published landmark clinical data for its multiple myeloma treatments. The company is trying to move further into complex biologics with these developments. And as exciting as this might be, I also think about the company’s intention to separate the orthopedics business within the next 2 years. I really liked JNJ exactly for this boring part of the whole product portfolio. Interestingly, recent reports from mid-February suggest JNJ might be pivoting from a spin-off to an outright $20 billion sale of this unit to private equity. I will monitor the situation closely.

Portfolio Changes & Visa Deep Dive

I doubled the position in Visa this month. Visa is currently trading at metrics that remind me of previous lows. A P/E at 29, the EV/EBITDA at 21 and the FCF yield is at almost 4%. Markets are pricing in a mixture of headwinds and future disruption fears for the company. This includes lower credit card issuance in the US due to tightening consumer credit, a rise of stablecoins as alternative payment means or cheap domestic payment solutions like WERO in the EU (influenced by successful examples like PIX in Brazil).

A few thoughts on this topic:

Domestic payment systems such as PIX (Brazil) and WERO (European Union) will likely only replace very low-margin, day-to-day transactions for V and MA. Think of your daily groceries (if at all) or the sandwich at the small deli next to you. Since its launch 2020 PIX has surpassed the combined number of credit and debit transactions in Brazil with a very high adoption rate of roughly 80% of the adult population. PIX or WERO is not about the hotel or flight you are booking or the shopping you’re doing on your holiday abroad. These are the high margin transactions for credit card companies. Coming from abroad you also cannot use these systems anyway. From the consumer perspective these systems are debit systems, there is no cashback, no fraud protection, no bonus points, no miles, no lounge access, no insurance benefits. The incentive to use them is 0, even if the merchant gives you a discount of 0,5 or 1% you may still want to collect those points.

The widespread use of instant payment systems such as PIX, WERO or others will or can hurt Visa and Mastercard, but these transactions are not the main driver of revenues for them.

To mitigate risks arising from stable coins, Visa has integrated USDC on the blockchain directly into operations. With a USDC settlement, banks benefit from faster funds movement over blockchains, seven‑day availability and enhanced operational resilience across weekends and holidays without any change to the consumer card experience. Banks are ready to use it and Visa is simply adapting.

“Visa is expanding stablecoin settlement because our banking partners are not only asking about it - they’re preparing to use it,” said Rubail Birwadker, Global Head of Growth Products and Strategic Partnerships, Visa. “Financial institutions are looking for faster, programmable settlement options that integrate seamlessly with their existing treasury operations. By bringing USDC settlement to the U.S., Visa is delivering a reliable, bank‑ready capability that improves treasury efficiency while maintaining the security, compliance and resiliency standards our network requires.”

Source: Visa

Visa is actively adopting and open to new technologies.

This is what Jack Forestell, VISA Chief Product and Strategy Officer recently said at the Wolfe Fintech Forum:

...I'd say I've been doing this payment technology thing for a really long time, 20+ years, and I will honestly tell you, I have not stared into a bigger growth opportunity than what we have ahead of us in the development of the agentic web. See, agentic web broadly that then will turn into agentic commerce, turn into agentic payments. I haven't seen anything like this since the dawn of e-commerce itself in the late 1990s, early 2000s."

Over time we will see if either Visa (and me) are wrong or the market.

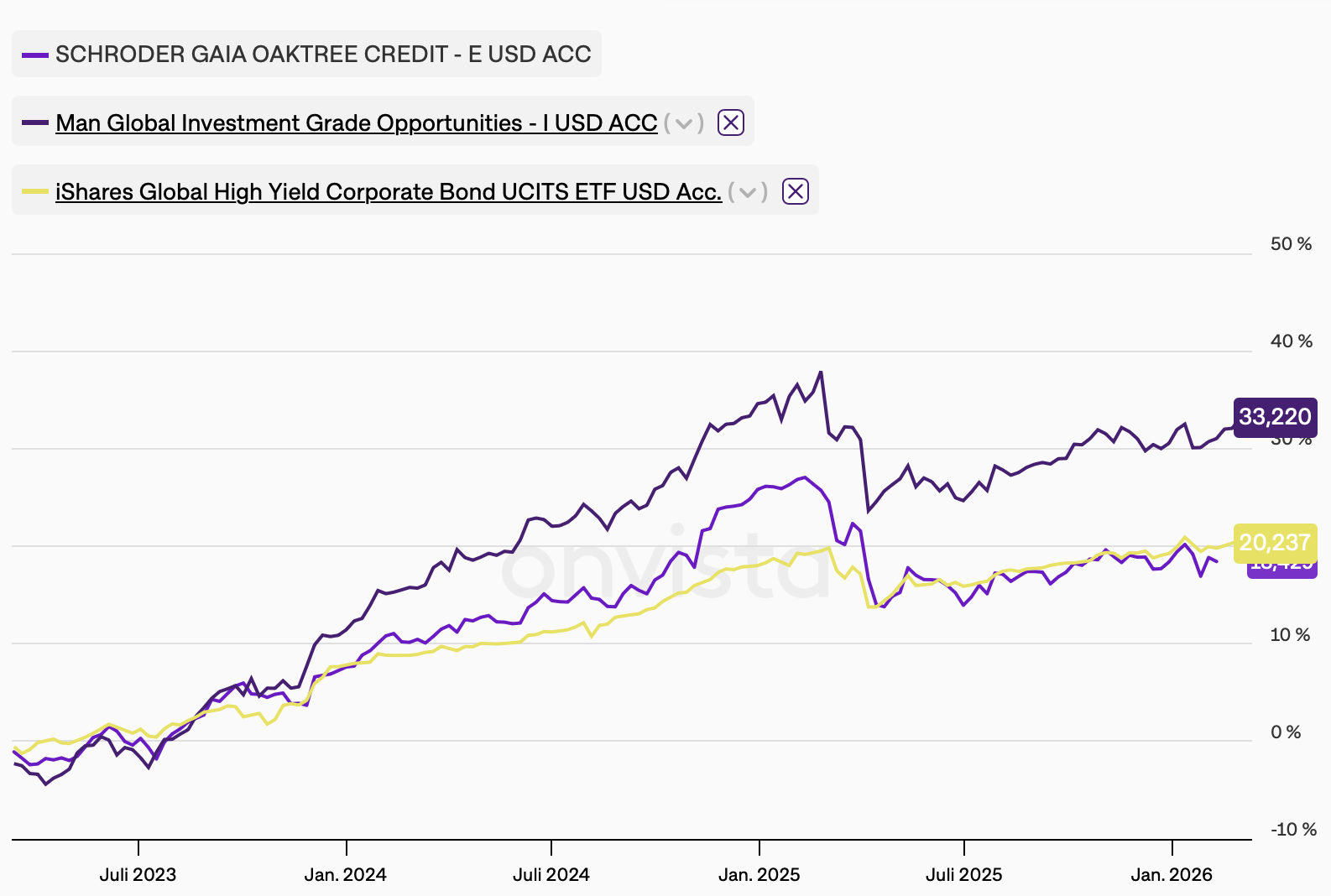

In the Diversifying Strategies segment, my investment in the Schroder GAIA Oaktree Credit Fund was converted into the Oaktree Global Credit Selection Fund (1.8% weight). The new fund has a similar risk profile to the one previously distributed by Schroder. GAIA Oaktree was a multi strategy credit fund, specializing in allocating capital across various segments of the credit spectrum, including high-yield bonds, structured credit (such as real estate debt), convertibles, and emerging market debt. The other credit fund in the portfolio is the MAN GLG Global Investment Grade Bond Fund. Is has a similar risk and return profile like the old GAIA fund and the new Oaktree product. All of these credit funds are correlated to high yield corporate bonds as visible below, although they have higher returns (and higher volatility).

Instead of keeping two separate positions I may consolidate the credit risk in the portfolio into only one of the funds for simplification purposes.

Another position I may change is the BlueBalance Global Opportunities Fund, which is a boutique macro hedge fund from Austria. The position is only 1% of the portfolio and therefore too small to really have an impact, so I am considering to sell it and buy some more of the Brevan Howard feeder fund (BH Macro). BH Macro is listed in London as a closed-end investment fund. It provides access to the Brevan Howard Master fund and invests primarily in global macro themes with trading strategies across asset classes like fixed income, forex. Returns are somewhat uncorrelated to global equity markets and especially during downturns BH Macro generally shines.

Thank you for reading along.

This publication is for informational purposes only and does not constitute investment advice or an offer to buy or sell any security. Past performance is not indicative of future results.