From The Desk - Week of December 08 2025

A small moment of pride for Europe, and a reminder of where real leadership still sits.

This week’s From The Desk comes a little early. But I have an important family event over the weekend, so I will not be able to update this later.

This week I spent time with the latest Merrill Lynch Capital Market Outlook. It made me very proud as a European:

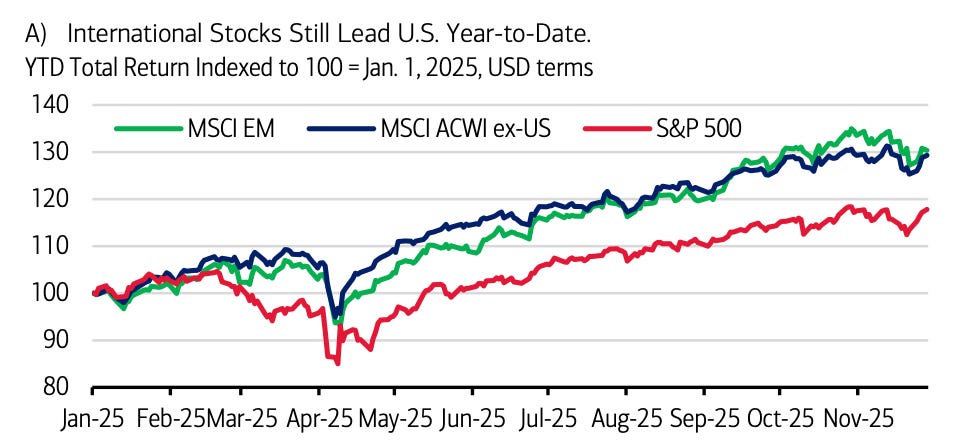

Ex-US equities have outperformed this year (in USD).

In a world dominated by the S&P 500, this is remarkable in itself. According to Merrill Lynch, emerging markets and Europe both delivered 30%+ year-to-date gains in USD terms, with ACWI ex-US up 29%.¹

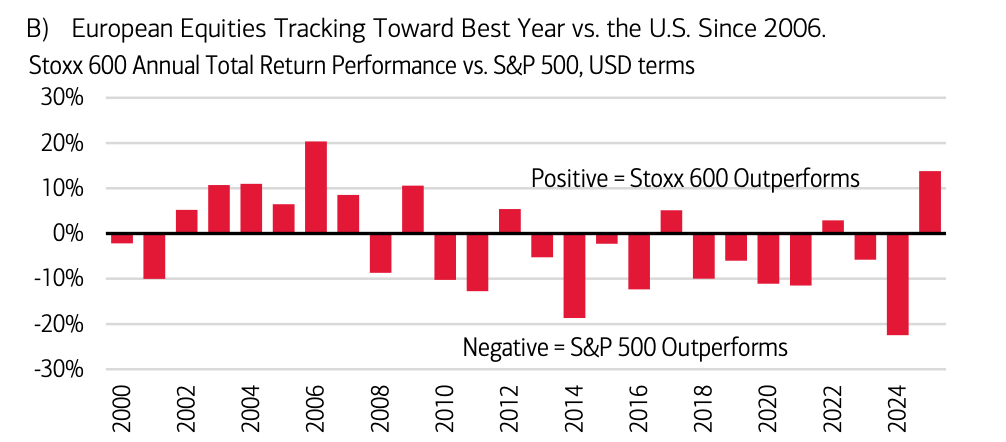

Europe, in particular, is on track for its best year relative to the S&P 500 since 2006.

Together with strong EM performance, this is a reminder that global diversification is not the worst idea. For me, personally, the U.S. remains the market where I expect the best performance over the long run (still). It offers companies the best conditions to thrive. Less regulation certainly than in Europe, flexible workforce, access to top notch graduates and research, energy security, and easy, quick access to one the most powerful consumer markets in the world.

Is this Europe’s moment to shine?

No. There was a brief “Europe is back” moment early this year. Then the narrative softened again.

Structurally, Europe has:

more consumers than the U.S.,

excellent universities

global leadership in selected industrial niches,

and huge untapped productivity potential.

But at the same time, Europe is held back by:

fragmented fiscal policies,

mismatched pension systems,

inconsistent capital-market structures,

slow decision-making,

and a regulatory environment that is not built for speed.

I often think about Europe like a family business run by brothers, sisters, cousins, and grandparents. Name one successful business run this way. It’s a nice story, but it rarely scales.

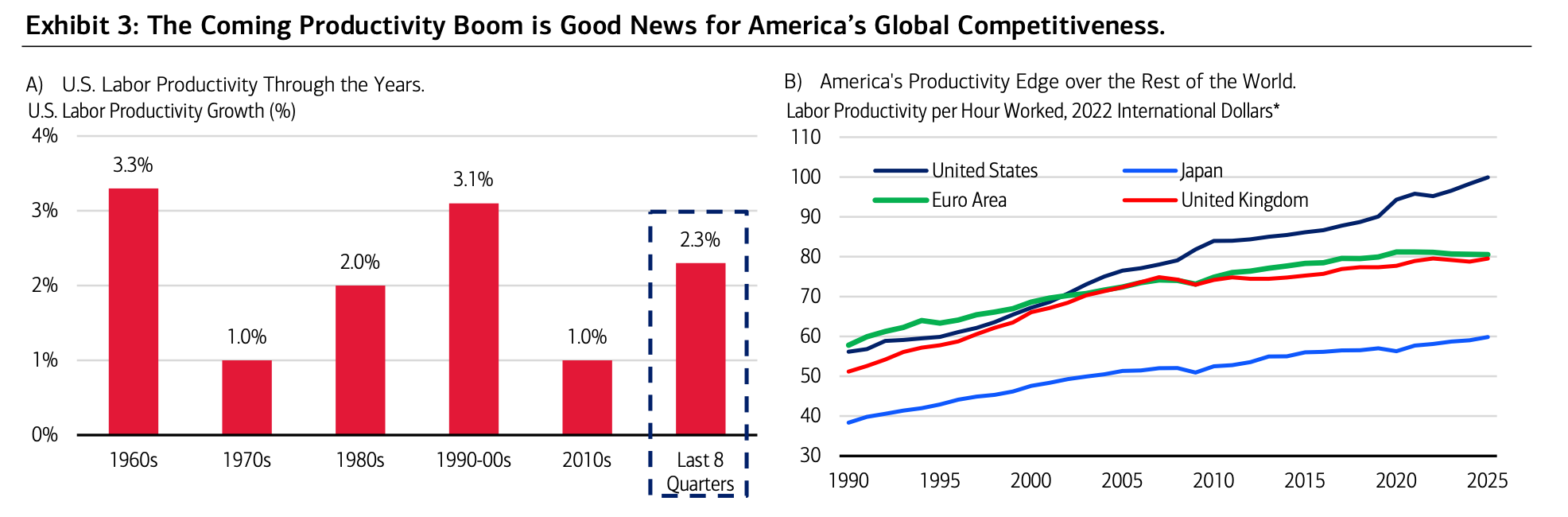

Speaking of productivity:

“Meanwhile, Exhibit 3B illustrates how far and fast the U.S. has run ahead of its global peers this century when it comes to boosting labor productivity. Simply put, there is America, and there is the rest of the world, although China’s expanding use of AI, robotics and other means of automation have raised the labor productivity of China’s labor force this century. America’s early embrace and adoption of AI, in our opinion, will maintain the U.S.’ productivity lead over the rest of the world. For investors, consider some non-U.S. assets but core portfolios should be anchored in U.S. securities of all shapes and sizes, in our view.”

What Merrill Lynch wrote here is pretty similar to what I wrote above already. The U.S. still remains No. 1.

Grant’s Interest Rate Observer: Foreign Buyers Are Stepping Back

Jim Grant flagged something interesting this week:

“European-domiciled ETFs tracking the U.S. stock market swung to net outflows over the past month — a dynamic seen only a handful of times since 2020.”

Add to that:

U.S. CAPE > 40 for only the second time in history,

U.K. pension funds with £200 billion in assets reducing U.S. equity exposure,

foreign allocations quietly easing off the S&P 500.

This is anecdotal, but it matters. Global investors are no longer treating U.S. equities as “the only game in town.”

Check in Later

As we move towards year-end, I will revisit the topic of U.S. vs. Ex-U.S. assets again and we will see where we stand going into 2026 again.

Have a great week.