From The Desk - Week of December 15 2025

Mixed Markets, Merrill Lynch on Affordability, and a fund letter from TIGER VALUE

Global markets this week (via T. Rowe Price)

I really like to read the T. Rowe Price Weekly Reviews. Here is a summary of what they saw: Global markets ended the week mixed, reflecting a familiar late-cycle tension between easing policy and valuation concerns. In the U.S., equities initially pushed to new highs after the Fed delivered its third consecutive rate cut of the year, but gains faded as technology stocks sold off on renewed doubts about AI-related capital spending paying off. Longer-dated Treasury yields moved higher, underscoring that easing policy does not automatically translate into lower long-term borrowing costs.

In Europe, equity markets were broadly flat, with policymakers signaling a prolonged pause rather than further rate cuts, while economic data continued to point to sluggish growth. Japan stood out modestly on expectations of a Bank of Japan rate hike, reflecting stronger wage and inflation dynamics, while China’s markets drifted lower amid persistent deflationary pressures and only incremental progress on reflation efforts. Overall, the picture remains one of policy support at the short end, but rising selectivity and skepticism at the long end of markets.

Source: T. Rowe Price

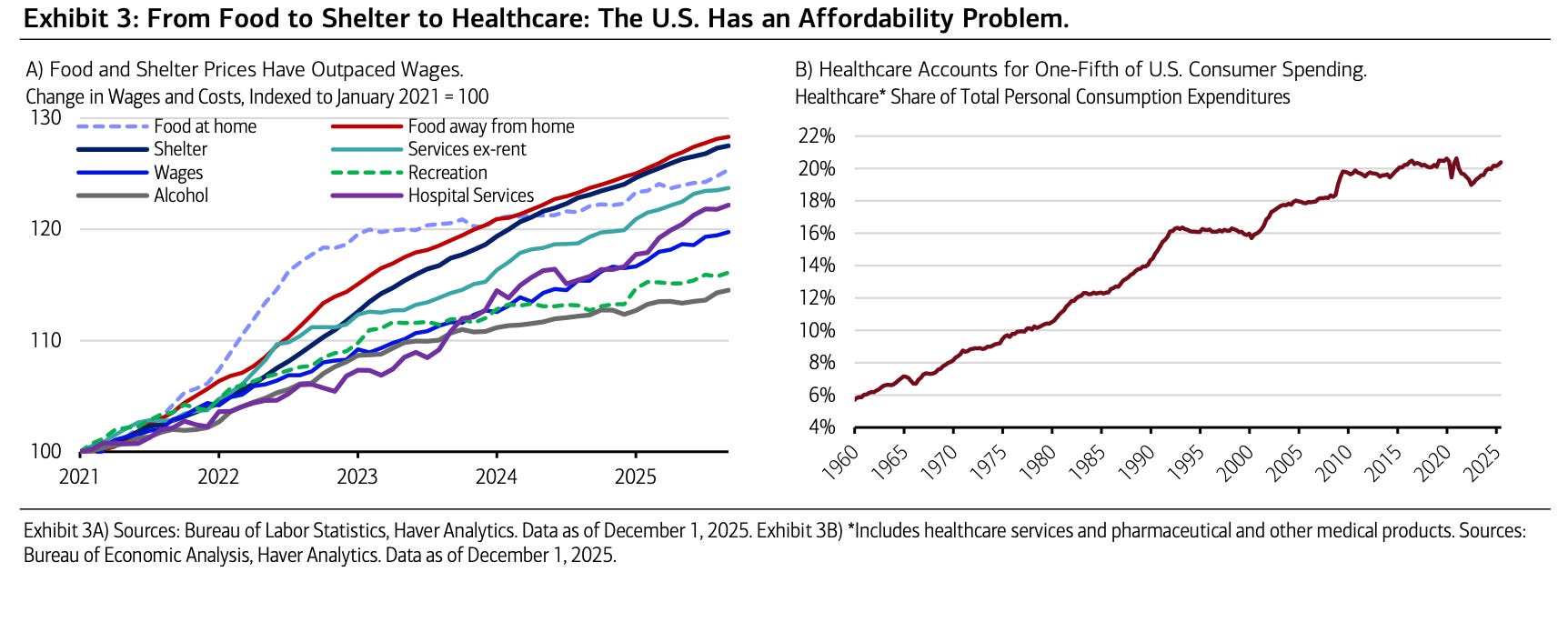

Merrill Lynch: affordability and markets in 2026

A section of Merrill Lynch’s Capital Market Outlook that stood out to me focuses on affordability, and how it may shape financial markets in 2026:

“On the economic front, the risk is that consumer spending comes in weaker than expected next year, as higher prices for goods and services crimp the budgets of both lower- and higher-income households. The fact that affordability is impacting higher-income consumers is evident from the fact that Dollar Tree, after reporting that 3 million additional households shopped in their stores in Q3, noted that, of those, 60% had incomes over $100,000.”

The core message is: higher prices and higher interest rates are colliding. The consumer is not doing well. Housing affordability remains stretched, corporate refinancing costs are structurally higher than in the last cycle, and governments are running persistent fiscal deficits (and will continue to do so). Even if central banks continue to cut policy rates, affordability constraints may limit how much demand can respond. Also let us keep in mind that yields on the long end of the curve are rising reflecting caution in the bond markets.

For markets, this implies a less forgiving environment:

asset prices will likely need to justify themselves with cash flow, pricing power, and balance-sheet resilience,

businesses with large amounts of debt may see re-ratings

and valuation dispersion could remain elevated.

Have a look at the chart below:

A few personal notes on housing affordability, but also housing as an investment here in Europe: I can only speak for the German city I live in. Prices remain elevated, owners simply refuse to lower them and my gut feeling is that housing markets are stagnating. Over time one will have to give in, either the buyer or the seller. As an investment overall cap rates are not very attractive here. Gross yields are roughly at 2-3% for large cities like Munich or Hamburg. It is hard to find investments in rental apartments that will have a yield greater than 4 or 5% on invested capital using leverage. Add to that rent controls by the government and you scare every international housing investor away from your domestic housing markets.

Tiger Value Fund: themes they are watching for 2026

Although I am not invested, I continue to read the Tiger Value Fund letters with interest. The Fund holds a portfolio of long and short positions focused on European equities.

Key themes they highlight in their November 25 fund update for 2026:

Rotation away from crowded AI momentum toward value, defensives, and under-owned small- and mid-caps

SMID recovery potential driven by stabilizing fund flows, attractive valuations, and rate cuts

Infrastructure and capex-linked spending, including Germany’s €500bn investment program

Defense and security upcycle, with global spending expected to rise materially into 2030

Digital infrastructure, IT services, and automation, benefiting from AI adoption without paying peak AI multiples

Energy transition and power infrastructure, particularly grids, storage, and efficiency solutions

On the short side: companies structurally challenged by AI, weak governance, aggressive accounting, or consumer pressure

I wish you a wonderful week!