Listen to Yourself

Zoetis (ZTS) made new lows this week. It reminded me that even the finest companies can be poor investments when valuation drifts too far from reality. Quality matters, but price still writes the story.

Chipotle Mexican Grill (CMG) also sold off sharply after earnings. The brand remains one of the few fast-casual concepts that still feels relevant to today’s health-conscious consumer. Fresh ingredients, fast execution, strong brand equity. But even good stories need growth. Same-store sales have stalled while the multiple remains rich. Bill Ackman owns it through Pershing Square, and it is a name I would like to revisit myself.

This week I listened to Bill Ackman on Value Investing with Legends. A great conversation about how he built Pershing Square and his broader principles on business and investing. One anecdote stood out: the moment he realized he must ultimately make his own decisions, even after listening carefully to others.

Take advice, but own the judgment. No one else bears the result.

Ackman also reminded listeners that most good investment cases are simple. There are no XXL spreadsheets, you just need visibility on where future earnings come from. I try to simplify things the same way. Predictability of earnings is an under appreciated quality of good businesses. It makes life as an investor so much easier. But even there, humility matters. Just ask Diageo. Predictable as it seemed, consumer habits shifted (at least the market thinks so), and the “easy” story stopped compounding. We’ll see that lesson again, somewhere else soon.

Thematic Report: The System Can Handle the Debt — It Can’t Handle the Politics

This week’s Tiny Family Office report examined sovereign debt and political paralysis.

Most Western governments, remain fiscally stretched yet structurally unable to reform. Adjustment will come only when markets or demographics force it.

Spoiler alert: demographics won’t. For the next 10–15 years, the majority of voters will belong to the dependent and retired population — the very group most reliant on state transfers. The deeper issue may be the growing loss of trust in capitalism among younger people. When they feel excluded from moving up by working hard, buying a home, building prosperity. The system begins to lose legitimacy. If that promise cannot be kept, the real problem is not fiscal, but political stability itself.

For investors, this environment favors businesses with strong balance sheets, and pricing power. Government debt will end up in the income statement of companies in the end.

The AI Conglomerate

Grant’s Interest Rate Observer relayed an unusual Bloomberg story:

Bill Pulte, director of the Federal Housing Finance Agency, said that Fannie Mae and Freddie Mac are exploring ways to take equity stakes in technology companies.

“We have some of the biggest technology and public companies offering equity to Fannie and Freddie in exchange for partnering with them… because of how much power they have over the ecosystem,” he said.

It’s a curious sign of the age. Mortgage agencies are flirting with tech equity. If this AI-era blending continues, we may soon see a web of cross-ownership across industries, where the line between policy, finance, and private capital becomes increasingly thin.

What I’m Reading / Watching / Listening To

Longleaf Partners Global Fund Commentary 3Q25: A global fund with a focus on real assets and consistent FCF growth. Positions in Rayonier and PotlatchDeltic reminded me of the timberland companies I had a look at a few years ago. Something worth revisiting.

Podcast: Bill Ackman on Value Investing with Legends

An entertaining, grounded conversation. I enjoyed it very much.

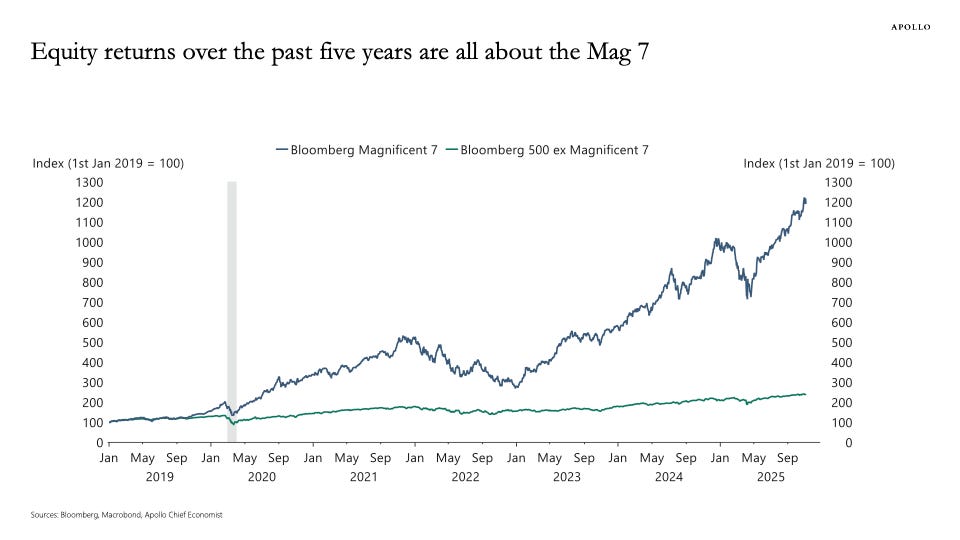

Chart of the Week

Thorsten Slok highlighted how equity returns over the past years have been dominated by the “Magnificent Seven”.

The chart is striking. But even even excluding those seven, the rest of the index has risen from 100 to roughly 250 since January 2019 which is not too bad either.

Market Recap

S&P 500: - 1.63 % (w/w)

MSCI ACWI: - 1.32 % (w/w)

STOXX 600: - 1.3% (w/w)

10-yr Yields: U.S. 4.1 % | U.K. 4.35 % | Germany 2.65 % | France 3.46 % | Japan 1.67 %

Gold: ≈ US $ 4003 / oz (−0 % w/w)

Brent Crude: ≈ US $ 63 / bbl (−1 % w/w)

Shutdown ≠ Selloff: The U.S. government shutdown (now day 40) constrains data flow more than risk appetite. Markets remain fixated on AI and liquidity, not Washington drama. First signs of a deal appeared today.

Hype Check: Michael Burry resurfaced on X with early 13F filings showing puts on high-multiple AI names (NVDA, PLTR). The market still “buys the dip,” but leadership breadth remains thin.

Valuation matters, so does judgment. Both start with listening to yourself.

I wish you calm markets and a good start into the week.