Intro

This week connected three themes: China’s industrial rise, the coming robotics cycle, and the state of housing affordability. All of it framed by Buffett’s final letter which is a reminder of what matters beyond the noise.

China’s Industrial Machine Is Pulling Away

I received a letter from Quantex this week discussing robotics and China. I still have a very, very tiny residual position in the Quantex Value Fund that I’m not willing to sell. I enjoy reading their letters, the research, the conclusions. Sometimes I believe the managers are a bit too negative and they sell too many of the businesses they buy. I’m more of a collector in this context…

But the Quantex letter made one thing uncomfortably clear:

China is dramatically accelerating its robotics buildout.

Key facts:

China installed 295,000 industrial robots in 2024

Robot density is 2× the EU

57% of new robots are now domestically produced

China added 426 GW of electricity generation in one year. Mostly coal of course while some countries are shutting down nuclear power…

(Source: Quantex citing Jefferies)

To reinforce this picture, I’m citing from an article called “China, the United States, and the AI Race” from the Council on Foreign Relations:

China’s Ministry of Industry and Information Technology estimates that by the end of 2025, over 60 percent of large Chinese manufacturers will have adopted some form of “AI + Manufacturing” integration, and thousands of “AI-empowered” factories have already been certified nationwide. The country’s 14th Five-Year Plan calls for “comprehensive intelligent transformation” of industrial production, with AI embedded across 70 percent of key sectors by 2027, 90 percent by 2030, and 100 percent by 2035.

Now contrast this with Europe. We are struggling with high industrial energy costs, especially in Germany. Our carmakers are losing competitiveness. And when we talk about the future of AI datacenter power demand, energy availability and build-out speed matter enormously.

When I read articles about the “AI race,” the narrative is always China vs. the US.

Where is Europe?

China and Asia-Pacific remain attractive as macro themes. Governance issues in China are real, and I personally would never touch an individual Chinese stock.

Still, as long as we don’t stumble into a Taiwan conflict, for me it makes sense to own businesses selling into China and here I mean especially those offering brands and products that China cannot really replicate because they are not “sexy” enough. Brands. An LVMH bag will always be an LVMH bag, I believe.

The Next Big Theme: Robotics After AI

Robotics will follow the AI–datacenter buildout as the next major industrial cycle or at least the next hype wave.

Because of that, I often think about owning the enablers of robotics rather than the end products. The companies that supply the mission-critical components, whose parts cost a fraction of the robot but are almost impossible to replace. Price increases barely matter to the customer.

A few examples after short research:

SKF or Timken – precision bearings

Fuchs Petrolub – specialty industrial lubricants

Just examples, but this is the direction I’m exploring.

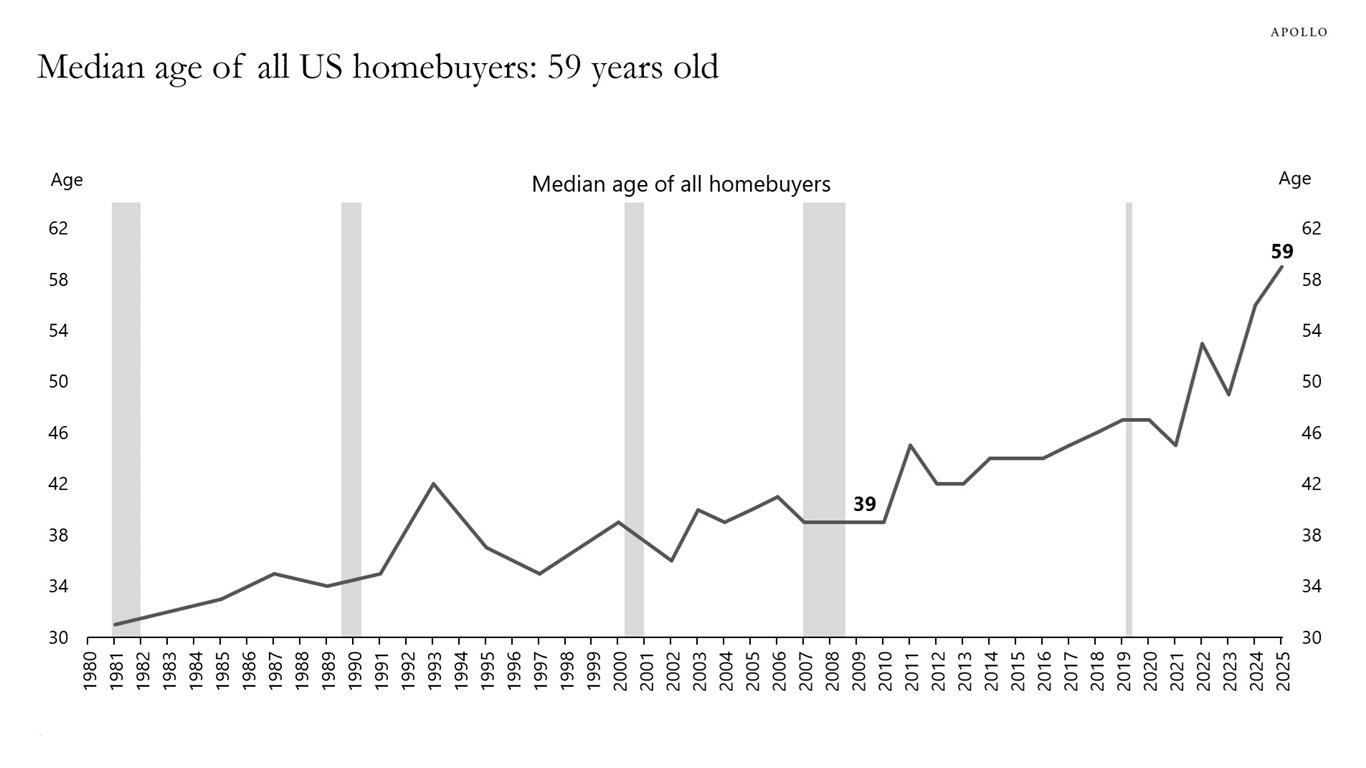

Housing: The Chart of the Week

Thorsten Slok’s “Daily Spark” chart showed something remarkable:

Median age of US homebuyers:

2010: 39

2025: 59

(Source: Apollo – Daily Spark, Thorsten Slok)

Source: Apollo - The Daily Spark

Now mortgage lenders are proposing solutions straight out of a dystopian novel mentioned in this article by The Guardian. A 50-year mortgage is not financing. It’s an intergenerational debt instrument. I’m not sure what to think of it.

If we consider long-run purchasing power and government debt dynamics, the real value of a USD 2–4k monthly mortgage payment in 30 years might be laughably low but in my opinion that doesn’t solve affordability today.

I don’t think extending the maturity of debt fixes the housing crisis neither in Europe nor in the US. The only thing I’m certain of is that banks will like it.

Buffett’s Final Letter: “I’m Going Quiet”

Warren E. Buffett released what is effectively his last major shareholder communication at Berkshire Hathaway. You can find it here.

A few lines stood out:

“I was born lucky - healthy, reasonably intelligent, white, male, in America.”

“Greatness does not come from money or power.”

“Kindness is costless but priceless.”

“The cleaning lady is as human as the Chairman.”

It’s a strangely emotional document. I had to chuckle a few times. But actually it reminded me of something that really touched me.

The recognition that capital matters, until health or life pulls everything into focus.

Anyone who has ever faced the fear of losing a parent, a child, or their own health knows exactly what I mean. I personally have had the experience in my life and found this absolutely devastating.

You cannot buy health. Full stop. Only when you lose it or you actually have a reason to fear losing it do you realise its full value.

The world feels insanely fast-paced right now. Everything is new every day. Markets, headlines, noise. We spend our days thinking about money and prices. But maybe we should be thankful a little more often for our health, and keep our loved ones a bit closer tonight as we realise how truly wealthy we already are.

Closing thoughts

Pretty boring week in markets overall, though the noticeable move was higher government bond yields in Europe, the US, Japan and the UK. , especially on the long end. Equities were pretty much flat. Let’s see how this sets up into year-end.

I wish you a wonderful week!