Welcome to 2026.

The year has already started in a way that once again confirms what some have come to call “the new normal”: a world where initially unusual, and unsettling things happen, and markets learn to live with them.

Donald Trump already removed Maduro from power. We have seen U.S. forces board a Russian-flagged vessel just days ago. On X, many immediately declared that “red lines had been crossed.” And yet nothing happened. No immediate escalation, no direct confrontation.

This is the world we are operating in now. I do not expect 2026 to be any calmer. At the time of writing, I am also watching developments in Iran closely.

Despite initially aggressive trade rhetoric and potential “tariff wars”, and policy uncertainty, the global economy has proven more resilient than many feared. President Trump’s America First agenda and trade confrontations dominated much of 2025, alongside the AI investment boom, rising geopolitical tensions, and Europe’s historic rearmament (and lacking growth).

Global growth remains close to 3%, broadly in line with recent years.

We enter 2026 from a relatively solid starting point. With the so-called “Liberation Day” now behind us it is difficult to construct a near-term scenario where the global economy truly derails. Companies and economies adapt quickly.

There are a couple of major developments I will be watching particularly closely this year:

Can Germany Reignite Growth?

The loosening of the debt brake has opened the door to large-scale investment in defense and infrastructure. We are also seeing encouraging, and politically meaningful, steps in capital markets: a new German “micro” pension scheme based on equity investments and the creation of a small sovereign wealth fund. Americans may smile at the scale, but for Germany this represents a substantial shift.

Structural challenges, however, remain formidable:

An aging population

Unfunded pension obligations

Lagging productivity

Intensifying competition from China, particularly in automotive manufacturing

High energy costs, expensive labor, and a bloated bureaucracy

An Independent Federal Reserve?

Another key issue is the appointment of Jerome Powell’s successor as Chair of the Federal Reserve.

President Trump has been explicit in his desire for significantly lower interest rates. It is reasonable to expect that the next Fed Chair will be more receptive to White House preferences. That alone is not necessarily problematic as the Chair does not set policy unilaterally.

The risk lies elsewhere.

If markets begin to question the independence of the Federal Reserve, confidence could erode quickly, particularly in bond and currency markets. Long-term yields not (short-term) policy rates will be the signal to watch.

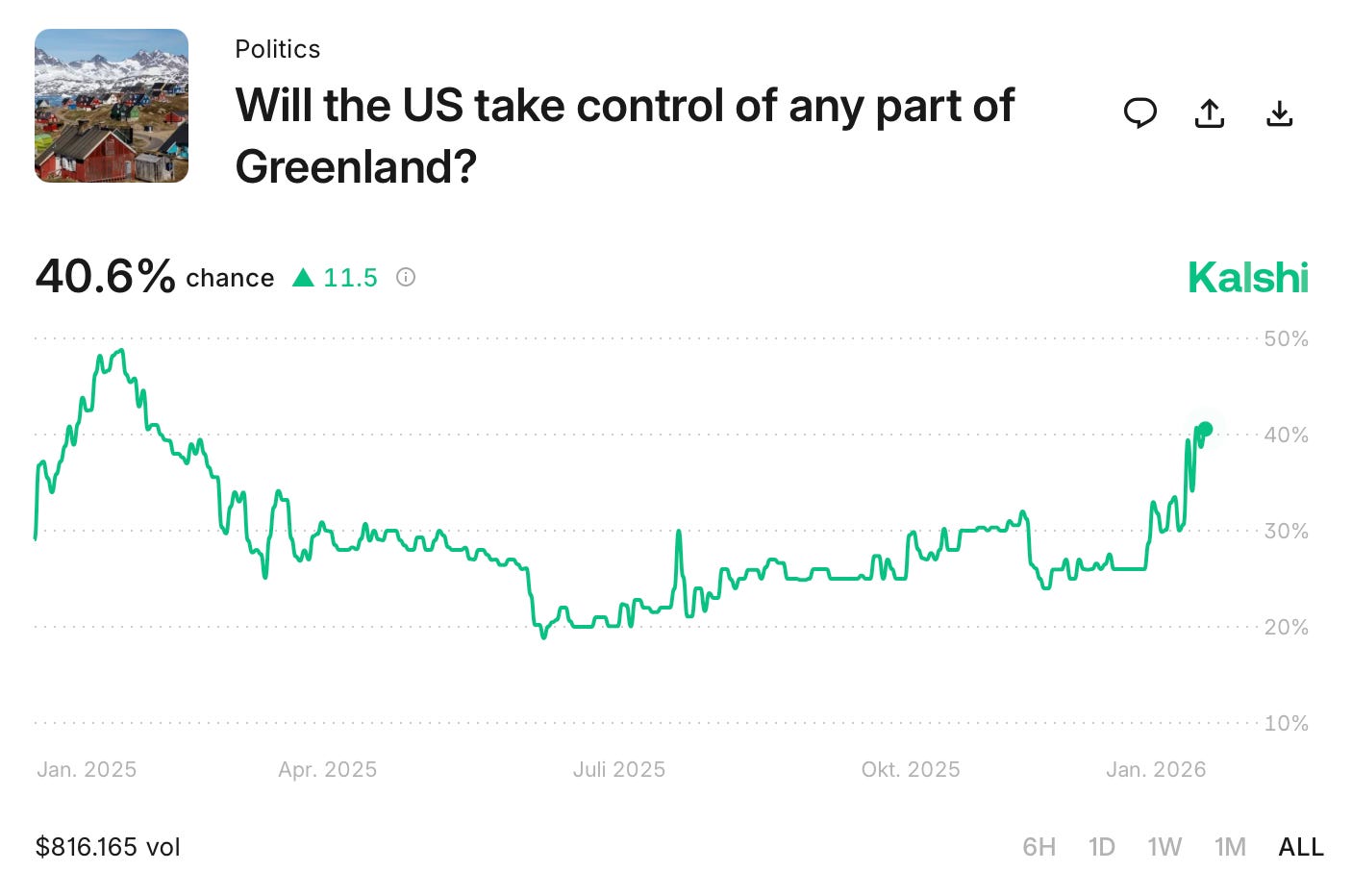

Greenland: Will Donald Trump follow through?

According to betting platform Kalshi, there is roughly a 40% probability that the U.S. will take control of some part of Greenland. This would have far-reaching implications for the U.S. role within NATO and Europe’s security architecture.

My personal view is that an agreement with Denmark will ultimately emerge: Europe will increase its presence in Greenland, and U.S. troops will likely do so as well. European leaders appear hesitant to meet Trump’s demands head-on, but Europe today is too fragmented and too weak to stand entirely on its own.

In a world undergoing a clear reshaping of the global order, steering away from the United States does not strike me as a prudent strategy.

Berkshire and the Long View

On a personal note, I will be watching Berkshire Hathaway closely this year as it is Greg Abel’s first year as CEO.

Over the Christmas period, I spent time reflecting on Berkshire’s role across themes such as grid expansion, energy security, a possible lender of last resort, and its unique portfolio of privately owned operating businesses.

There are very few companies globally that can play such a broad set of themes simultaneously. To me, Berkshire remains one of the greatest companies in the world, and I am proud to hold it in my portfolio.

The Portfolio

I have also partially introduced The Tiny Family Office portfolio, outlining a structure of roughly 70% equity investments and 30% alternatives, including hedge funds, insurance risk, credit, and gold.

👉 https://www.tinyfamilyoffice.com/p/introducing-the-portfolio

I encourage you to read it carefully.

I wish us all a healthy, thoughtful and fruitful year 2026.

Yours sincerely,

The Tiny CIO