The Tiny Family Office Portfolio

As an investor I always assume I will most likely be wrong all the time. This portfolio is not designed to be exciting. It is designed to survive, and compound, across cycles, regimes, narratives, and despite my own mistakes. It is not designed to achieve a performance of 15% annualized. I do not optimize for quarterly outperformance.

Most retail portfolios depend on a single bull market in stocks. I have built this portfolio to compound across various cycles, inspired by the endowment models of Yale and Harvard, but adapted for individual implementation.

Structure

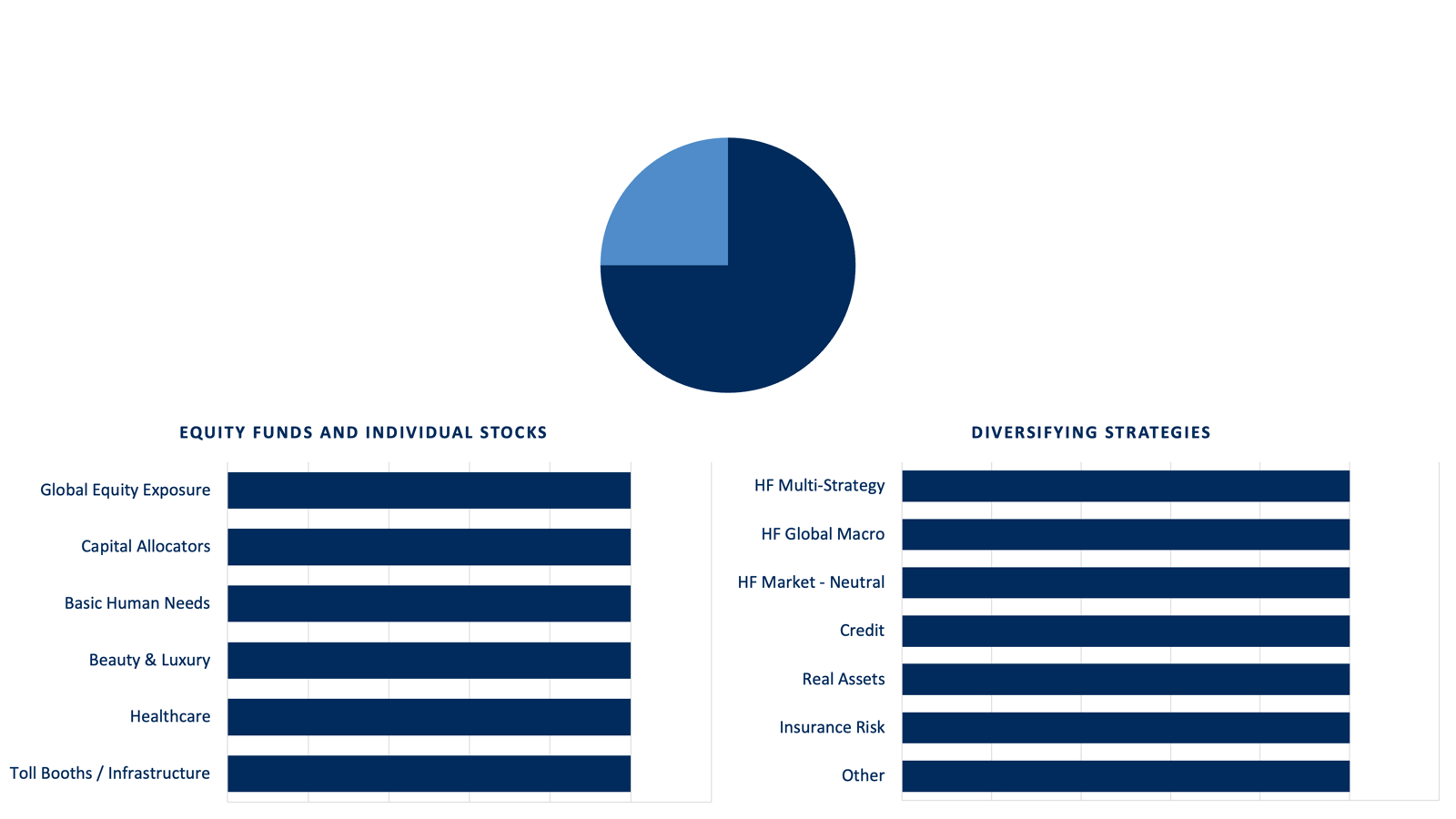

The portfolio is built around two functional sleeves, as visualized in the charts below:

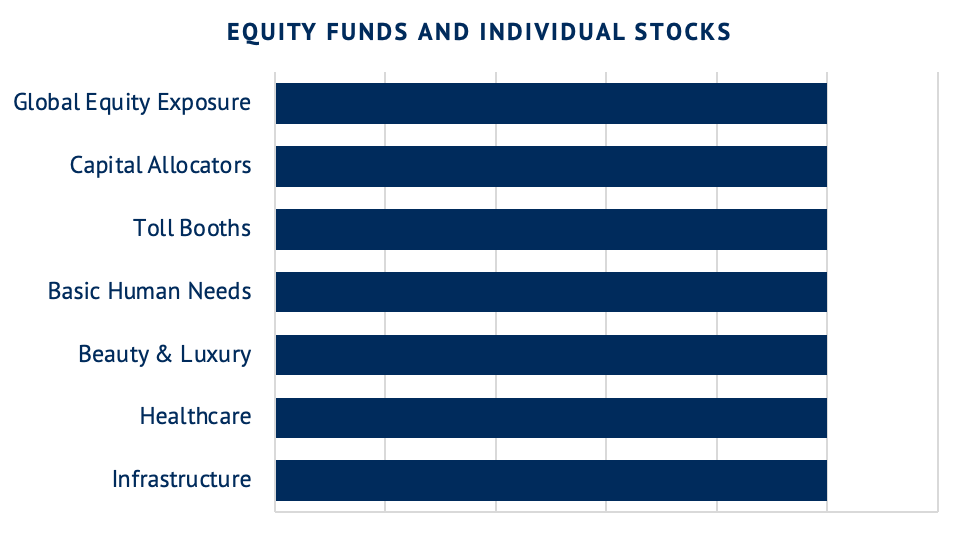

1. Equity Allocation (≈70–75%)

This is my portfolio part for long-term participation in global growth. The equity portfolio is intentionally conservative. The core consists of global equity exposure through an index fund. I also add individual companies based on my research. Rather than trying to predict the next technological wave, I focus on businesses that benefit from structural demand, high capital returns, and limited risk of disruption. The businesses in the portfolio can be categorized into a few functional categories such as capital allocators or toll booths of economic activity.

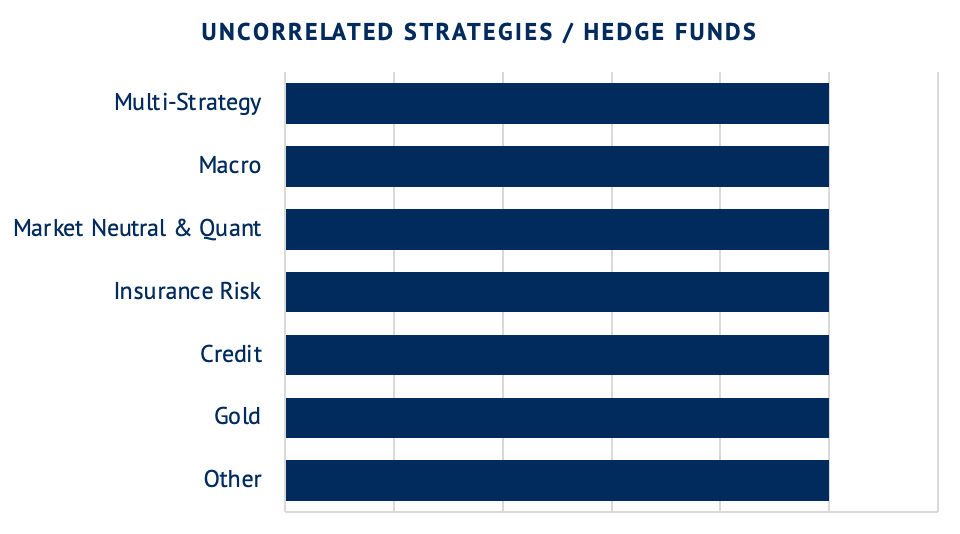

2. Diversifying Strategies (≈25–30%)

The purpose of this part is not return maximization, but the reduction of dependence on an equity bull market. It is designed to perform when equities fail, and markets get shaken. The inspiration to invest in alternatives initially came from David Swensen. It then developed through a savvy (finance) community, and was possible due to generous decision by my banks (thank you) to give me access to the funds. I have allocated to specialized vehicles typically reserved for much larger institutional investors. The portfolio consists of e.g. multi-strategy hedge funds, discretionary macro strategies or some long / short funds. Furthermore, I hold insurance risk exposure through cat bonds, I own credit and some gold or other commodities (real assets).

No single strategy works all the time, but together, they provide the resilience necessary to withstand environments where my traditional equity portfolio will struggle.

Principles & Constraints

I assume equity returns over the next decade will be lower than the last one.

I assume macro shocks will be more frequent, not less (Maduro just got extracted from Venezuela last night, while I was writing this post).

I assume I will change my mind slowly and publicly. The portfolio will change, too.

What I Avoid

Private Equity: I avoid the illiquidity and the extreme performance gap between top-tier managers and the rest. Also I believe access is really limited to the best funds.

Long-Duration Bonds: I avoid locking in capital for decades at low yields.

Crypto: I prefer assets with productive cash flows or a multi-century history.

Most importantly this portfolio is not static. Over time I will make changes to individual holdings and asset class weightings.

A Final Note

You may enjoy my weekly newsletter CIO Notes. I share a curated selection of what caught my eye in markets, what I read, or which podcasts I listened to. I also share insights from fund manager letters, industry research, and other sources currently influencing my decision-making as a capital allocator.

You can join the conversation by subscribing below.

Full allocations, changes, and commentary are shared in the Monthly Portfolio Letters.