From The Desk - Week of November 24 2025

A week of AI fatigue, cautious positioning, and one labour-market trend worth watching.

This week was another interesting one in the markets. Helaba captured it well in their weekly outlook: despite Nvidia delivering strong results, equities could not gain traction, and even traditional safe havens like bonds and gold failed to attract flows.1

T. Rowe Price’s weekly update tells the same story2:

In the U.S., Nvidia posted record revenue and raised guidance again. The stock opened higher and closed down 3% on the day, dragging indices with it.

In Europe, the STOXX Europe 600 fell ~2.2%.

Japan’s AI-related names sold off, and tech weakness pulled the Nikkei and TOPIX lower. At the same time, the Japanese government unveiled a JPY 21.3 trillion stimulus package, pushing the 10-year JGB yield to a 17-year high and weakening the yen.

We remain in that strange zone between year-end positioning and macro uncertainty neither bad enough nor good enough to set a clear tone. A possible peace deal in Ukraine may change that, but apparently there has now been some confusion around the author of the peace plan according to an article from Reuters. I highly doubt a deal will be possible shortly.

Francois Rochon: The Mistakes That Matter Most

I listened to the Wealthtrack Podcast this week featuring Francois Rochon, founder of Giverny Capital. If you like to learn more about Rochon I genuinely recommend this interview here with him: Compounding Quality. What struck me wasn’t a clever mental model but a simple truth: his biggest mistakes were always the companies he didn’t own because they “looked too expensive,” and the companies he sold too early.

It’s the reason I almost never sell unless the business fundamentally breaks. Missing compounders is the silent killer of long-term returns. A −50% loss on a 2% position is an annoyance. Missing a potential 20-bagger is catastrophic, just invisible on performance statements.

TCI, Visa, and Why I Started a Position

I revisited a couple of 13F filings, and one stood out to me:

TCI Fund Management (Chris Hohn) increased its stake in Visa.3

That alone doesn’t make a thesis, but TCI is selective, valuation-aware, and genuinely long-term. Seeing them add made me revisit Visa myself.

I initiated a small position. This is not THE fat pitch yet but acceptable in the current market.

Valuation:

Visa trades around 23× EV/EBIT, back to its 2018 valuation range. Not cheap but far less demanding than the mid-30× multiples during 2021–2022. Based on a quick napkin valuation last week, even with revenue growing at only inflation + 1%, Visa can still compound EPS at 7–10% due to its structural buybacks and operating leverage. The conversion into free cash flow of each increase in revenues is superb.

Current market fears may be a slow-down in spending and economic activity, Walmart or Amazon launching own payment systems, European alternatives like Blik or Wero. They all look overblown (to me). There is a structural difference between building a payment method and building the global settlement rails. Visa is the latter, it is a brand that stands for trust, and yes I sometimes may switch to Paypal or other payment methods when shopping online but it doesn’t change my overall spending habit by taking my Visa, Mastercard or Amex.

The brand still stands for trust.

Magellan Filings: Transurban

I also reviewed filings from Magellan’s Infrastructure Fund and the Magellan Global Fund. One name stood out:

Transurban

One of the purest listed plays on long-duration toll road concessions globally. Built-in inflation linkage, recurring cash flows, and significant optionality if real rates stabilise.

It remains on my watchlist.

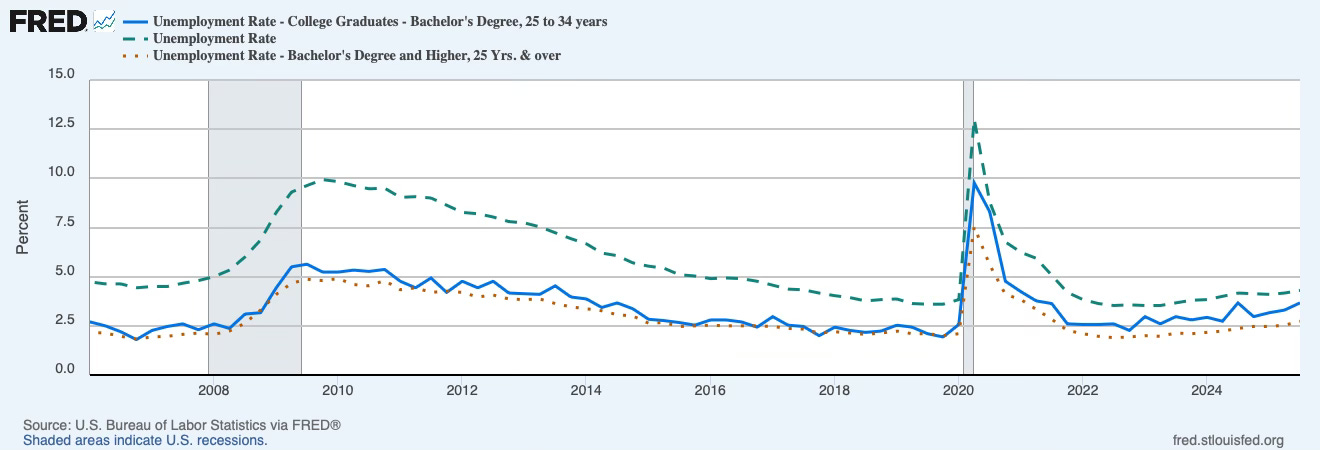

A Worrisome Trend: College Graduate Unemployment

One issue that increasingly worries me: rising unemployment among recent college graduates in the US.

Labor market softening is hitting recent college graduates especially hard. Data from the Current Population Survey show a troubling pattern for young workers who have recently graduated. Young college graduates between ages 23 and 27 are experiencing unemployment rates that average 4.59% in 2025—a stark contrast to the 3.25% rate this same demographic experienced in 2019.4

Figure 1 also shows an uptrend in the unemployment rate of people with a Bachelor’s aged 25 to 34. It is not too step so it does not indicate a full stop in the job market but looking at the data from 2008 unemployment also crept up slowly until it suddenly gapped.

This is something I will be watching closely during the next months along with other economic data.

I wish you a great start into the new week!

Helaba Research & Advisory, Wochenausblick, 21 November 2025, pp. 1–3.

T. Rowe Price, Global markets weekly update.

TCI Fund Management 13F filing, November 2025.

St. Louis Fed, Recent College Grads Bear Brunt of Labor Market Shifts.